Understanding and Improving Your Credit Score

Your credit score is key to your financial health. It’s a three-digit number that can affect your loan terms. A good score means lower interest rates and easier approvals.

Credit reports from Equifax, Experian, and TransUnion are the foundation of your score. They track your payment history and how much credit you use. Keeping an eye on your credit helps you catch problems early.

People with excellent credit can save a lot of money. Banks offer better deals to them. But, a bad score can make it hard to rent, buy a car, or get insurance.

Key Takeaways

- Credit scores range from 300 to 850, with higher scores indicating better creditworthiness

- Payment history contributes 35% to your credit score

- Credit utilization makes up 30% of your score – aim to keep it below 30%

- Length of credit history (15%), credit mix (10%), and new credit inquiries (10%) also impact your score

- Regular credit monitoring can help you spot and address issues quickly

What is a Credit Score and Why It Matters

A credit score shows how reliable you are with money. Lenders use it to decide if they can trust you. The FICO score, which is the most common, ranges from 300 to 850. This number is very important for your financial health.

Definition and Importance of Credit Scores

Credit scores come from your past money habits. They show if you’re likely to pay back debts. A high score means you might get better deals, but a low score could limit what you can do.

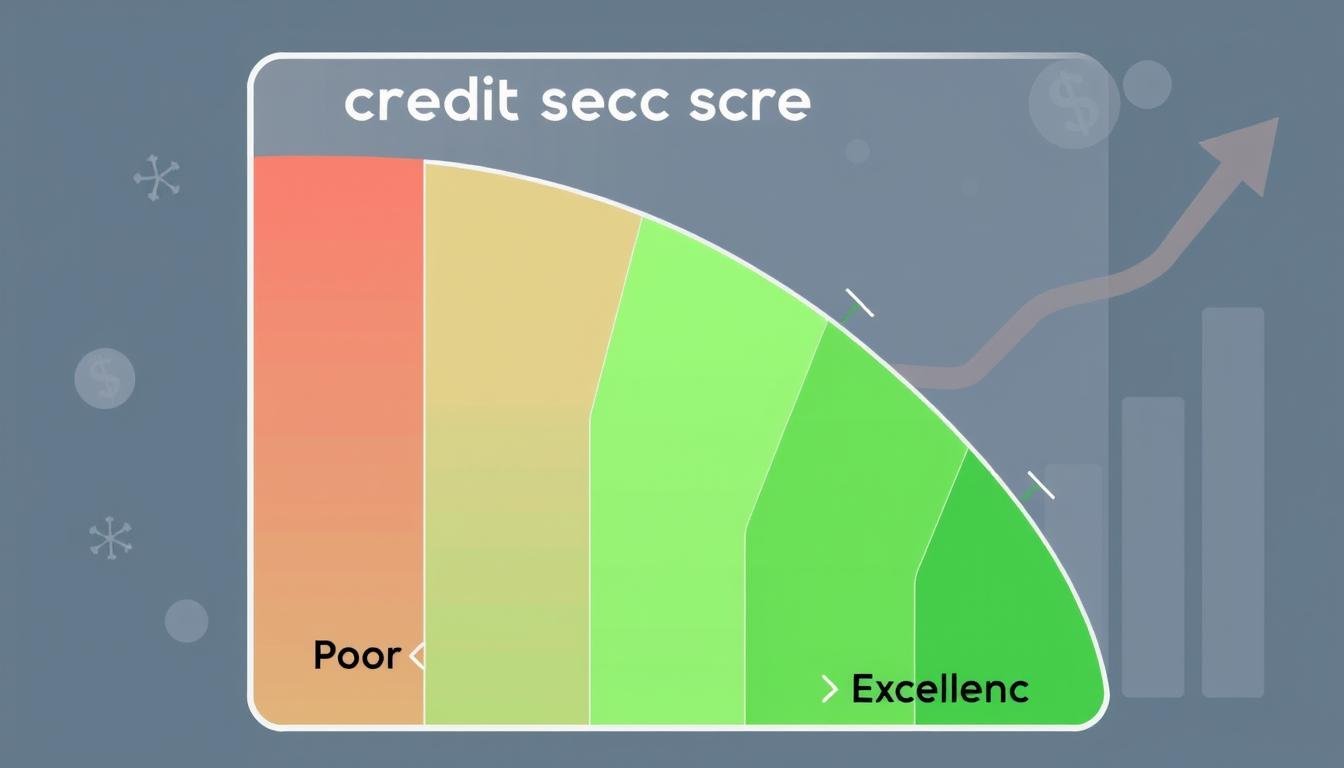

Credit Score Ranges Explained

Credit scores fall into different groups:

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

Try to keep your score above 670 to be seen as a good risk. Scores over 800 are top-notch and can get you the best deals.

Impact on Financial Opportunities

Your credit score affects many parts of your money life. It impacts your ability to:

- Get loans with good interest rates

- Rent an apartment

- Get approved for credit cards

- Pay less for insurance

A high credit score can save you a lot of money. It’s a powerful tool that can lead to better financial options. Knowing and managing your credit score is crucial for reaching your money goals.

How Credit Scores Are Calculated

Credit scores are key to your financial health. Knowing how they’re calculated helps you manage your credit better. Let’s explore the five main factors that affect your score.

Payment History: The Foundation of Your Score

Your payment history is 35% of your FICO score. It shows if you pay bills on time. Late payments and bankruptcies can hurt your score a lot. Keeping up with payments is the best way to improve your score.

Credit Utilization: Balancing Your Debt

Credit utilization is 30% of your score. It shows how much credit you use. It’s good to use less than 30% of your available credit. For example, if you have a $10,000 limit, try to use less than $3,000.

Length of Credit History: The Value of Time

The length of your credit history is 15% of your score. It shows your credit experience. A longer history usually means a higher score.

Credit Mix: Diversity Matters

Your credit mix is 10% of your score. Lenders like to see different types of credit. This shows you can handle various financial responsibilities.

New Credit Applications: Proceed with Caution

The last 10% looks at new credit applications. Applying for many accounts at once can seem risky. Each application can lower your score temporarily.

Understanding these factors helps you make better choices to improve your score. Remember, your score changes often. Positive changes in your credit habits can lead to a better score.

The Role of Credit Bureaus and Credit Reports

Credit bureaus are key to your financial health. Equifax, Experian, and TransUnion are the big three in the U.S. They gather and keep your credit history info.

Your credit report is packed with important stuff. It lists your name, address, Social Security number, and more. This info helps lenders decide if they should lend you money.

The Fair Credit Reporting Act makes sure reports are right. You can get your free annual credit report from each bureau at AnnualCreditReport.com. It’s smart to check these reports often for errors or identity theft signs.

| Credit Bureau | Free Reports | Additional Features |

|---|---|---|

| Equifax | 1 per year | 6 extra free reports until 2026 |

| Experian | 1 per year | Credit monitoring services |

| TransUnion | 1 per year | Credit lock options |

Keep in mind, each report might show different things because of different sources. If you find errors, tell the credit bureau and the source of the mistake. This keeps your credit history accurate and might boost your score.

Essential Strategies for Building Credit

Building a solid credit foundation is crucial for financial success. Whether you’re starting from scratch or looking to improve your credit score, there are several effective strategies to consider.

Establishing Credit from Scratch

For those new to credit, the journey begins with small steps. One approach is to open a store credit card, which often has more lenient approval requirements. Remember, the goal is to use it responsibly and make timely payments to build a positive credit history.

Secured Credit Cards and Credit Builder Loans

A secured credit card is an excellent tool for building credit. It requires a cash deposit as collateral, typically ranging from $200 to $500. This deposit becomes your credit limit, reducing the risk for the issuer.

Credit builder loans are another option. These loans, usually between $300 to $1,000, are designed specifically to help establish credit. The borrowed amount is held in a savings account while you make monthly payments, demonstrating your ability to manage credit responsibly.

Becoming an Authorized User

Being added as an authorized user on someone else’s credit card can give your credit a boost. The account’s payment history will appear on your credit report, potentially improving your score. However, it’s important to note that this strategy has limited potential to enhance your overall creditworthiness.

| Strategy | Pros | Cons |

|---|---|---|

| Secured Credit Card | Low risk for issuers, builds credit history | Requires upfront deposit |

| Credit Builder Loan | Specifically designed for credit building | May have higher interest rates |

| Authorized User | Can benefit from someone else’s good credit | Limited impact on overall creditworthiness |

Remember, consistency is key when building credit. Make all payments on time and keep your credit utilization below 30% for the best results.

“Your credit score is a reflection of your financial habits. Start small, be consistent, and watch your creditworthiness grow over time.”

Common Credit Score Mistakes to Avoid

Building a strong credit score takes time and effort. But, a few missteps can undo your progress quickly. Let’s look at common mistakes that can harm your score and how to avoid them.

Missing Payment Deadlines

Late payments can hurt your credit score a lot. Payment history is 35% of your FICO® Score, making it key. Even one payment 30 days late can hurt a lot.

These late payments stay on your report for seven years. This can have a lasting negative effect.

High Credit Utilization

Credit utilization is important, making up nearly 33% of your score. It’s key to keep your credit card debt under 30% of your limits. High balances can show financial stress and lower your score.

Closing Old Credit Accounts

Your credit history length affects up to 15% of your score. Closing old accounts can shorten your history and lower your score. It also reduces your available credit, which can increase your utilization ratio.

Keep older accounts open and active. This helps maintain a longer credit history.

- Avoid applying for multiple credit cards in a short time frame

- Don’t ignore your credit reports – check them regularly for errors

- Steer clear of maxing out your credit cards

- Think twice before co-signing a loan

By avoiding these mistakes and using credit responsibly, you can improve your score. A good credit score can lead to better financial opportunities and savings.

Monitoring and Protecting Your Credit Score

It’s important to keep an eye on your credit score for your financial health. Credit monitoring services make it easy to track changes and spot issues. They alert you to new accounts, inquiries, and other activities that could affect your score.

Regular checks can help find errors or signs of identity theft early. You can get free annual credit reports from each major bureau. Many credit card companies also offer free credit score updates, helping you stay informed.

To protect your credit, consider a credit freeze. This locks down your credit file, making it harder for criminals to open new accounts in your name. It’s a strong defense against identity theft, but remember to lift the freeze when you need to apply for credit.

| Credit Score Range | Category | Impact |

|---|---|---|

| 300-579 | Poor | Difficult to get approved for credit |

| 580-669 | Fair | May face higher interest rates |

| 670-739 | Good | Qualify for better terms |

| 740-799 | Very Good | Access to excellent rates |

| 800-850 | Exceptional | Best rates and terms available |

By staying vigilant and using these tools, you can keep a healthy credit score and protect yourself from financial fraud.

Credit Repair and Recovery Strategies

Fixing your credit score takes time and effort. It’s doable with the right steps. You need to tackle negative items on your report and plan to boost your score over time.

Disputing Credit Report Errors

Wrong info can hurt your score. It’s key to check your reports often and fix mistakes. Winning a dispute can really help your score.

Working with Credit Counselors

Credit counselors can help manage your finances and improve your score. They assist in budgeting, negotiating with creditors, and teaching about credit.

Debt Management Plans

Debt management plans are great for those with many debts. They roll all debts into one payment, often with lower interest rates.

| Strategy | Potential Impact | Time Frame |

|---|---|---|

| Disputing Errors | Immediate improvement | 30-90 days |

| Credit Counseling | Gradual improvement | 6-12 months |

| Debt Management | Significant improvement | 2-5 years |

Remember, fixing your credit score takes time. Bad marks can stay on your report for 7-10 years. But, their effect weakens over time. Making on-time payments and using credit wisely can show big improvements in a few years.

Conclusion

Understanding and improving your credit score is key to reaching long-term financial goals. Credit scores range from 300 to 850, and aiming high is best. Credit bureaus look at payment history and credit use most.

To boost your financial health, pay on time and keep credit card use under 30%. Having a mix of credit types and long accounts helps too. Remember, improving credit takes time and effort.

Checking your credit report often helps catch errors and identity theft. Good credit habits and avoiding mistakes lead to better financial chances. Steps like using secured cards or being an authorized user help build a strong credit profile.

Your dedication to managing credit well will not only raise your score but also improve your financial health. Stay informed, stay active, and see your efforts lead to a brighter financial future.

Source Links

- How to Improve Your Credit Score Fast

- Your Guide to Understanding and Improving Your Credit Score

- A Guide to Understanding and Improving Your Credit Score – Eastern Savings Bank

- What Is a Credit Score & Why Is It Important? | Equifax

- What Is a Credit Score? Definition, Factors, and Ways to Raise It

- How Is My Credit Score Calculated?

- How are FICO Scores Calculated? | myFICO

- How Are Credit Scores Calculated? | Equifax®

- Understanding Your Credit

- Understanding Credit Reports: How It Is Used | myFICO

- Credit Reports and Credit Scores

- How to Build Credit – Experian

- How to Improve Your Credit Score in 7 Steps

- Avoid These 5 Credit Mistakes To Raise Your Credit Score | Truist

- 7 Common Credit Mistakes and How to Avoid Them

- Common Credit Score Mistakes: 8 Pieces of Credit Advice to Avoid

- Understanding Your Credit Score: Strategies to Build and Increase Credit

- Understand your credit score

- How to Improve Your Credit Score: Tips for FICO Repair

- How to Improve Your Credit Score Fast

- How to Improve Your FICO Score | myFICO

- The Complete Guide to Understanding and Improving Your Credit Score | Upgrade

- Tips on How to Improve Credit Score | Equifax